Weekly Market Review 12/07/2018

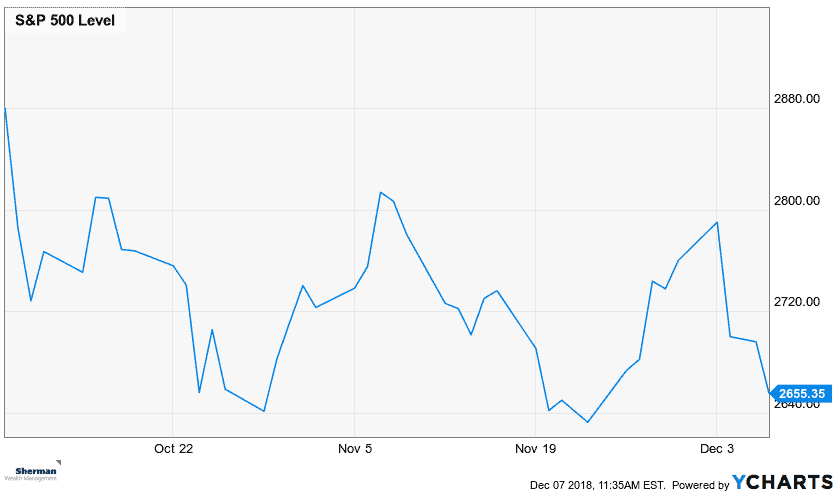

We experienced more of the choppy environment in equities this past week. Although these types of swings are more common than many realize (remember, the low volatility environment of 2017 was the real anomaly), we understand that large down days in the market can be bothersome. Most of the drama occurred early on Monday, after positive news that the US and China were inching closer to a truce on trade. As expected, the market didn’t end up buying into the hype after having the “rug pulled out from under them” with similar news being released over the past couple of months and the market selling off after each quick jolt. To make tensions worse, we saw more political chest-puffing, when the CFO of Chinese Tech giant Huawei was detained in Canada on Tuesday night. However, according to the White House, the trade talks and the arrest of the Huawei executive are separate issues altogether. The conflicting positive and negative news has kept us in a large trading range over the last two months, as you can see below.

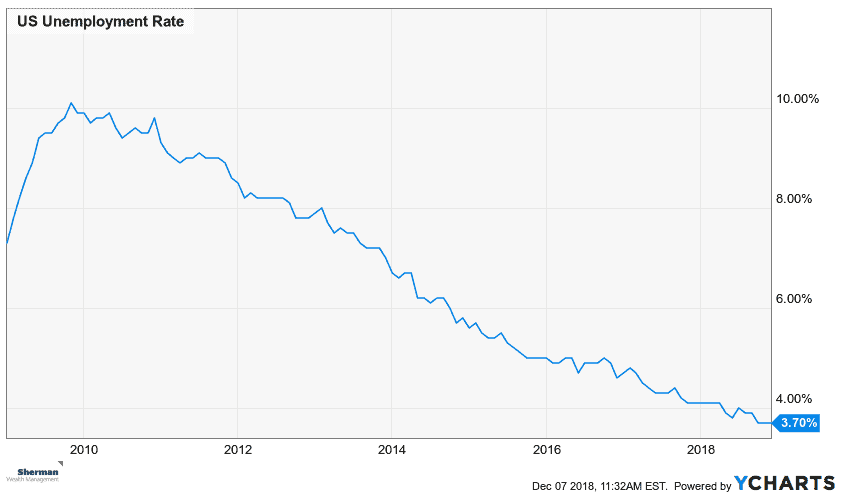

The US unemployment numbers posted a decent increase this past week, with non-farm payrolls increasing for the 98th month in a row. This is by far the longest streak of month-over-month job growth in history. Average hourly earnings also saw a small bump. The overall unemployment rate still stands at 3.7%, the lowest since 1969. Interestingly enough, a separate gauge that includes discouraged workers and those holding part-time jobs for economic reasons, sometimes called the real unemployment rate, rose from 7.4% percent to 7.6%. I would also like to take this time to point something out for those of you who may be hearing (or reading) a lot lately on the yield curve and how it relates to the US economy.

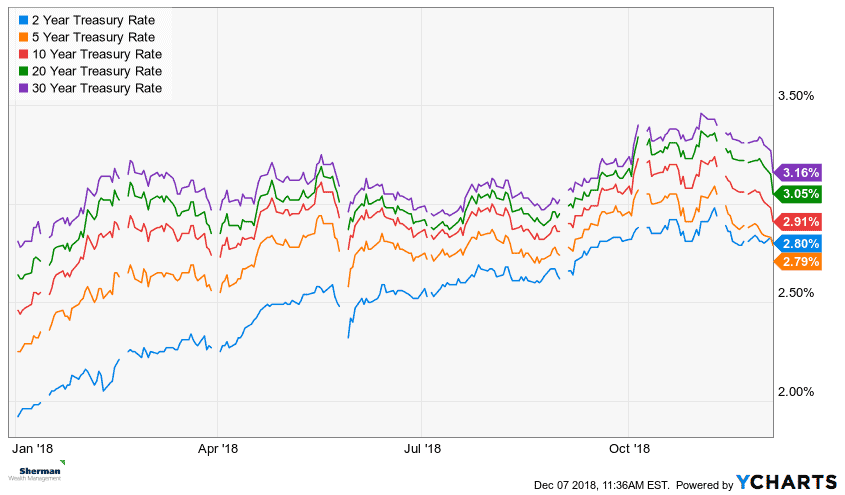

US interest rates continue to move lower following Fed Chairman Powell’s speech in which he felt that rates were “neutral” in accordance with where we are in the economic cycle. In layman’s terms, he says the Fed sees the current stream of economic data as remaining positive and thus there is no need to rush to raise interest rates, which would theoretically keep the economy from “overheating”, or growing too quickly. This should help damper fears for prospective homebuyers, as many have felt they’d “missed the boat” in regards to purching a home in the near future since mortgage rates had been on the rise

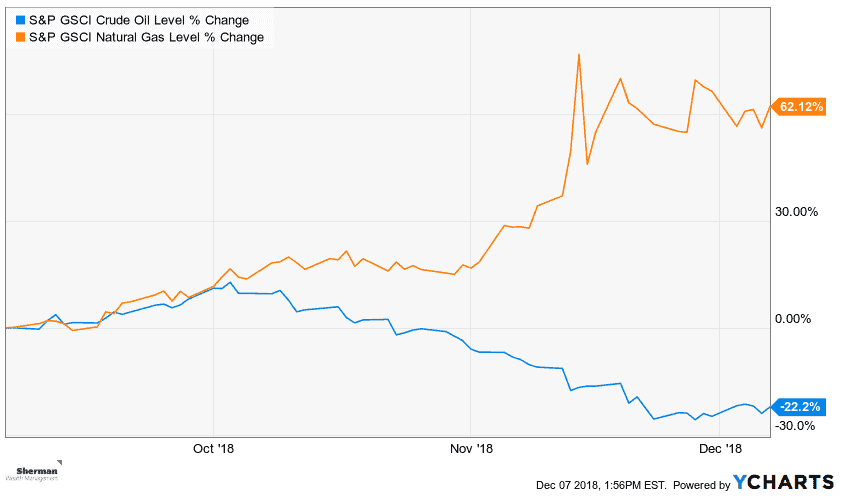

Two closely-tracked energy commodities (due to the fact that they are commonly purchased by a large number of households) have been moving in opposite directions lately and continue to do so. First off, crude oil prices have fallen from $76 to $50 per barrel recently, which should cause some relief at the pump for consumers. In fact, national gasoline prices fell to $2.46/gallon, a new low for 2018. A main cause of the lower prices has been the massive over-production here in the US. On the other hand, natural gas prices have seen a large spike over the last few weeks, in large part due to the lowest stockpiles of gas in nearly a decade. So, while you may be saving money when you fill up your car for a long road trip over the holidays, you may see a higher natural gas than usual as we go further into the winter months.

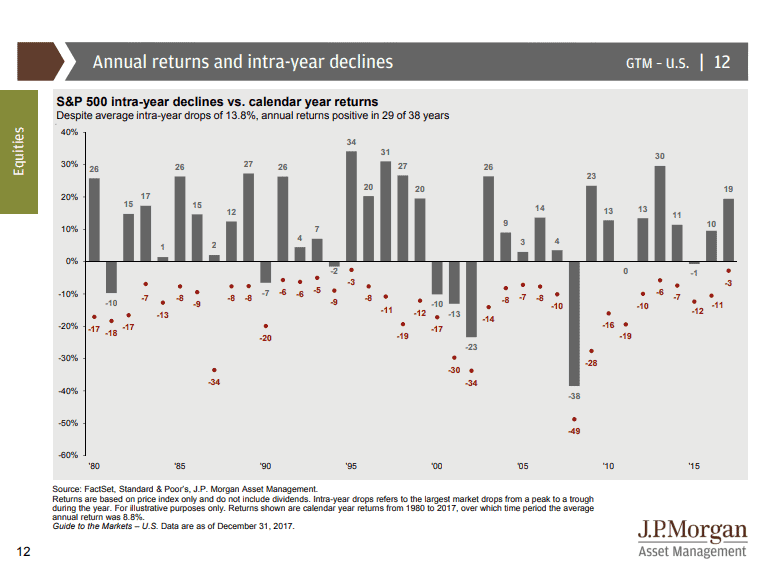

If you are feeling a little antsy over the recent market volatility, I would like to bring your attention to the chart below. The average intra-year drop on the S&P 500 is roughly 14%. So far this year we have experienced two declines, one of 12.8% (January – February) and one around 11.3% (October). Both are below the average. These types of swings are experienced on an annual basis. Due to the fact that 2017 was such a low volatility year (as mentioned above), recency bias has kicked in and has many believing that the 2018 environment is seeing above-average fluctuations. It is not. However, if your goals for your assets have changed, or if you believe your risk tolerance may not be in line with the drawdown you’ve seen in your portfolio recently, this is a great opportunity to let us know.